Is the winter of austerity ending?

Global markets have been focusing on US rate cuts over the past few months. But investors are increasingly looking to governments to stimulate growth, with a record 57% of fund managers saying fiscal policy is too restrictive, according to a recent survey of fund managers by Bank of America Merrill Lynch.

As rates descend below zero in Europe and Japan, the impact of cutting interest rates is fading. Central banks need help — and will to a much greater extent when the next recession comes. Fiscal policy could provide that boost, but it might not be forthcoming barring a recession. Although cross-party support is growing for Green New Deals, they’re more of a future hope than a present reality, so low growth and ultra-low rates look set to remain for 2020 at least.

Danger ahead

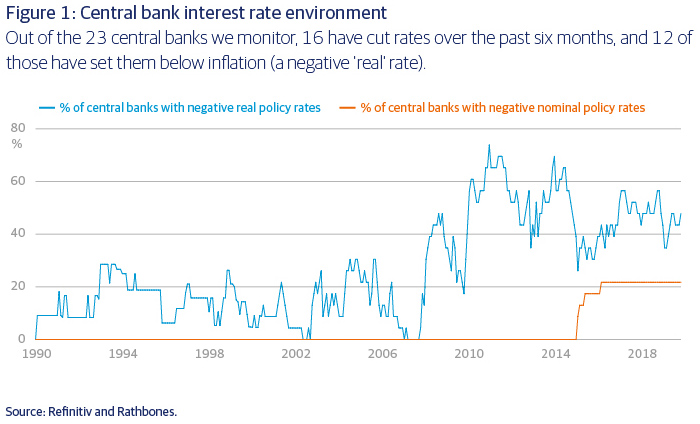

Of the 23 central banks we monitor, 16 have cut rates over the past six months, and 12 of those have set rates below inflation (negative real rates). More extraordinarily, five of them have set rates below zero, including the European Central Bank (ECB), which presides over the world’s third-largest economy (figure 1).

The evidence collected so far suggests that cutting rates when the starting point is already near or below 0% can still stimulate the economy, but to a lesser degree than when rates are significantly above zero. Moreover, monetary policy may become even less effective as rates go further into negative territory.

The conventional wisdom is that lower rates eat into bank profitability by squeezing the gap between what they pay to borrow funds and what they charge to lend them out (what’s known as net interest margin). It’s reasonable to expect bank lending to become more muted the more negative rates become, as declining profitability limits banks’ ability to make profitable loans, and/or causes them to pass on less than 100% of central bank rate cuts to their customers. (So far this has only been a problem in Switzerland.)

There are other reasons to think that the response to monetary policy just ain’t what it used to be. First, bank lending has become less responsive to policy rates since the regulatory changes made after the financial crisis to strengthen bank balance sheets. Second, there is widespread evidence of a lower propensity to invest and a higher propensity to save, despite extremely low rates. That may be due to structural issues like changing demographics and rising wealth inequality, but whatever the reason, a lower propensity to invest also constrains the response to rate cuts.

Fiscal policy to the rescue?

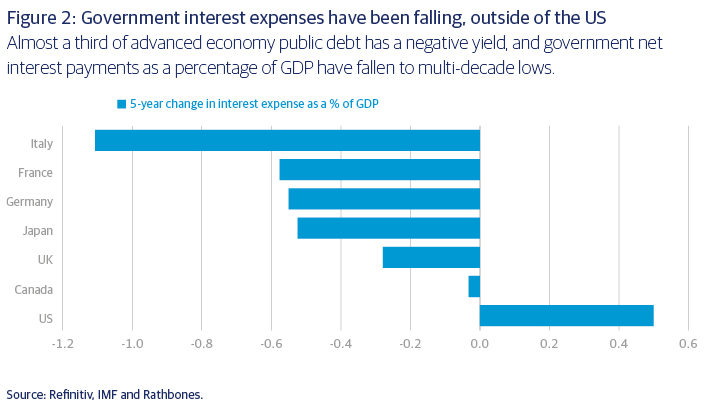

Low or negative interest rates mean lower borrowing costs for governments. Almost a third of advanced economy public debt has a negative yield, and government net interest payments as a percentage of GDP have fallen to multi-decade lows. Most major economies have plenty of fiscal space before investors traditionally worry about debt sustainability — in other words, before debt servicing costs rise beyond the sum of GDP growth and the primary deficit, which excludes interest payments (figure 2).

Yet most governments haven’t taken advantage of this fiscal leeway, which is a shame because it could make up for what’s lacking from monetary stimulus. In fact, several studies suggest that ‘fiscal multipliers’ (how many dollars of GDP growth arise from every dollar of fiscal expansion) may be much larger than usual when policy rates are at 0%. But there are potential issues.

Critics of fiscal policy highlight three risks: it threatens fiscal sustainability, the public sector is a poor allocator of capital, and government borrowing crowds out private investment. We’ve dealt with debt sustainability above. Regarding the second rebuke, we agree that wasteful spending is a risk, particularly due to the vested interests of politicians. But any pretension about the superiority of private sector capital allocation can be dismissed with three words — global financial crisis. Not to mention the serious problems of declining productivity and rising inequality.

The evidence on ‘crowding out’ is very mixed. Broadly speaking, there’s evidence that government borrowing to fund day-to-day expenditure can crowd out private borrowing, and borrowing to run state-owned companies is usually found to crowd out private enterprises in the same industry sector. But there’s also plenty of evidence of the opposite — ‘crowding in’. For example, government borrowing to invest in productivity-enhancing projects, such as infrastructure, can encourage more private investment because a more productive economy means higher potential returns. Crowding in can also occur if the banking or corporate sector is dislocated in some way — the hangover from a banking crisis perhaps?

The bottom line is that timing matters. Fiscal multipliers tend to work best when demand is deficient and there are no bottlenecks in the supply chain and other inflationary pressures.

Is now the time?

The German government knows it. When we asked about the possibility of imminent fiscal policy in October, the Head of the Public Finance Division at the Bundesbank said now is not the time: crowding out will occur and fiscal multipliers might be zero, and the government risks wasting its fiscal space.

This explains why the climate package Berlin unveiled in September — widely touted to be Germany’s version of a Green New Deal — turned out to be budget neutral: €54 billion of measures between now and 2023 funded by a carbon levy on domestic transport and heating.

An EU-wide Green Deal proposed by newly elected European Commission President Ursula von der Leyen would also be funded by taxes on the likes of fossil fuel and transport companies and other ‘polluters’. So far there is no indication that the EU would be willing to relax its tight budget rules to allow governments to help fund its ambitious plans with some fiscal largesse.

In some parts of the eurozone, the low-interest-rate environment is beginning to change the way fiscally conservative governments are thinking about debt. But only in the Netherlands, where public debt is just 50% of GDP, will it result in a major fiscal loosening for 2020. Although the French finance minister announced some giveaways in September, the headline budget is scheduled to tighten from -3.1% of GDP in 2019 to -2.2% in 2020 (see ‘Macron’s résistance’ on page 8).

In his bid to win the leadership of the Conservative Party, newly elected UK Prime Minister Boris Johnson promised a large UK fiscal stimulus. But a much more modest version is what made it into the party’s election manifesto. In fact, we would be calling it modest if this were a one-year budget, let alone a five-year plan.

Meanwhile, the chance of the much-anticipated bipartisan US infrastructure programme being enacted is lower than ever, with the Democrat-controlled House of Representatives voting to impeach President Donald Trump. As the November presidential election approaches, the Democrats won’t want to hand Trump anything — nothing raises the re-election prospects of an incumbent president like rising economic growth. Senate minority leader Chuck Schumer has promised that if the Democrats gain control of the Senate following next November’s elections, he “will introduce bold and far-reaching climate legislation”. But at this stage that remains a big if.

So the prospects are not good for significant fiscal stimulus across major economies in 2020, barring a recession. The tide of opinion is turning: for example, Germany’s version of the Confederation of British Industry is now lobbying for a loosening of fiscal restrictions, where in the past it has been a vocal advocate of balanced budgets. But the tide is turning slowly.