Diversifiers provide an antidote

Alternative strategies can help to protect portfolios in times of crisis

19 August 2020

Absolute return strategies, named for their purpose of providing a source of positive returns over the whole market cycle, have suffered negative press for some time. These funds, which we call actively managed diversifiers, have been criticised for underperformance relative to broader equity markets.

But the comparison itself is deeply flawed because these strategies are not aiming to outperform equity markets, nor should we expect them to. The whole idea of diversifiers is to provide sources of return that have a low, or even negative, correlation to equities. Measured correctly, we think these diversifying strategies have delivered through the recent turbulence and over the longer term. So how should we measure these strategies, and where and when is it appropriate to use diversifiers?

Dispelling diversification myths

According to traditional portfolio construction, investments are split across lower risk investments, such as cash and bonds, and riskier investments that have greater return potential such as equities. Weightings of each are determined by the investor’s appetite for risk, their tolerance for losses, and the market cycle. A traditional diversified portfolio would typically have a strategic allocation of 60% in equities and 40% in bonds. The proportions could be adjusted as appropriate at different stages of the market cycle. For example, equities could be increased during recovery phases and reduced in a downturn. The aim was to enhance the risk-adjusted returns of the portfolio. However, this approach was challenged by Harry Markowitz’s Nobel-prize winning work in the 1950s. A key insight was that holding different assets that are not positively correlated (i.e. don’t move in the same direction) will reduce the volatility of the portfolio. Intuitively this makes sense: if different assets are correlated, and therefore rise or fall together, they won’t provide the benefits of diversification that investors seek in times of market stress. To put it another way, there’s no use putting your eggs in different baskets if all the baskets are tied together; if one falls they all fall. More recent studies have shown that correlation between asset classes tends to increase during periods of market stress, as they did when COVID-19 started spreading across the world. This was also the experience of the global financial crisis, when corporate bonds came crashing down along with equities. We divide assets into three building blocks, which play different roles — liquidity (mostly safe-haven government bonds and cash), equity-type (such as shares, corporate bonds and emerging market debt) and diversifiers. This third category comprises assets that demonstrate a low or negative correlation to equities, particularly during periods of market stress. Using this ‘LED’ framework, portfolio diversification is built on risk protection, rather than relative and potential returns, and particularly on how different asset classes, instruments and funds behave at points of market stress. This helps us better understand the potential for losses at the overall portfolio level.Assessing performance

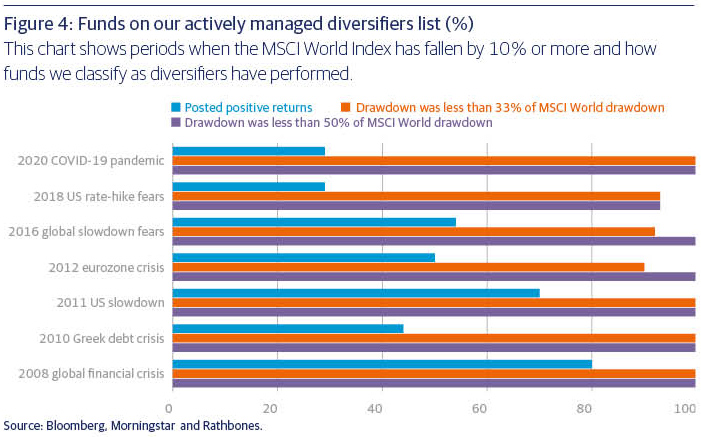

It is important to have some way of appraising performance, and in particular investors need to assess whether these actively managed strategies have smoothed returns within portfolios and provided protection during difficult periods in equity markets. Our research suggests they have, both historically and, in particular, during the recent panic selling as the coronavirus spread around the world, bringing economic activity virtually to a standstill. In this latest crisis, equity markets experienced their fastest-ever drop into bear-market territory (defined as a fall from the previous peak of 20% or more). At the height of the panic in late March, even the safest of assets, like government bonds and gold, were falling as investors were desperate for cash and selling everything. Figure 4 shows periods of drawdowns (falls from the previous peak) for the MSCI World Index of 10% or more, starting from the global financial crisis and including the pandemic so far, and how diversifiers held in a simulated portfolio fared in comparison. Encouragingly, a quarter or more of these funds posted positive performance in stressed periods, and nearly all funds across all stress periods had a drawdown that was less than a third of the MSCI World.

What about performance over longer time periods? We ran a simulation on a traditional 60/40 portfolio over the past 15 years using actual fund performance from Morningstar. This showed a correlation of 0.98 to a portfolio of 100% equities, 1.0 representing a perfect correlation. And, surprisingly, even a portfolio of 30% equities and 70% bonds would’ve had a correlation of 0.74 over the same period. This illustrates that the majority of risk within a traditional combined portfolio of stocks and bonds is equity-type risk.

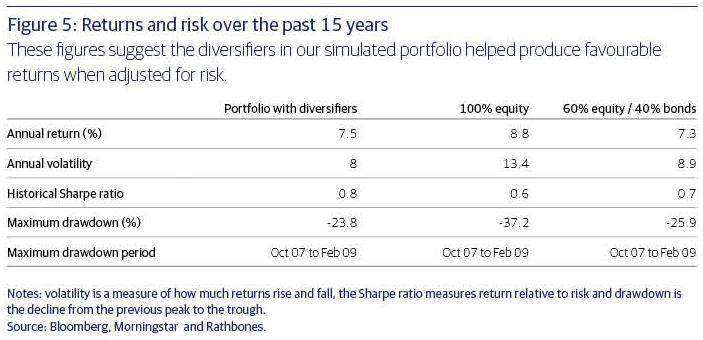

Figure 5 shows a historical comparison of various measures of return, risk and risk-adjusted returns for an equity-only portfolio, a 60/40 portfolio and our simulated portfolio including a strategic blend of diversifiers. The figures suggest the diversifiers within the simulated portfolio limited downside compared to the equity-only portfolio and the 60/40 blend of equities and bonds, took on less risk than the latter and produced favourable returns when adjusted for risk.What drives returns

What are the different types of diversifying strategies, their role in multi-asset portfolios and the conditions that might be conducive to positive performance?"We divide assets into three building blocks, which play different roles — liquidity (mostly safe-haven government bonds and cash), equity-type (such as shares, corporate bonds and emerging market debt) and diversifiers. This third category comprises assets that demonstrate a low or negative correlation to equities, particularly during periods of market stress."

Long—short equity, where managers can make a profit when share prices rise and others fall, is one of the most popular diversifying strategies, though some funds in this category track equities fairly closely and we wouldn’t consider them as diversifiers. The average stock market correlations have fallen dramatically over the past 18 months, which in theory should create better conditions for identifying winners and losers. However, managers may not get their stock-picking right. Event-driven funds seek to exploit pricing inefficiencies that may occur before or after a corporate event, such as an earnings call, bankruptcy, merger, acquisition or spin-off. If the aftermath of the pandemic leads to consolidation, where stronger companies snap up their weaker rivals to gain market share, these kinds of strategies may stand to do well. But ‘deal risk’ from regulatory or political challenges, for example, is an issue for event-driven strategies. Again, stock-picking is key to capturing returns from these anomalies. Global macro managers invest according to economic and political conditions in various countries. These funds experienced a rough patch in recent years owing largely to the absence of volatility in markets, but COVID-19 and other risks such as a hard Brexit or a global trade war could create opportunities. Commodity trading advisers (CTAs) — also known as trend-following funds — use derivative contracts across all asset classes to generate returns from market trends. Evidence so far suggests they have been successful in picking up some of the clear trends emerging from the pandemic, such as falling commodity prices, falling long-term yields and currency moves. Knowing what the various drivers are for the performance of the different strategies can help tilt portfolios toward the current opportunities. But the important thing is that these drivers are different from equity markets, and Figure 5 highlights the importance of maintaining diversification at the strategic level. The wide range of fund returns suggests that fund selection is key and can add real value over and above strategic and tactical allocation within diversifying strategies.