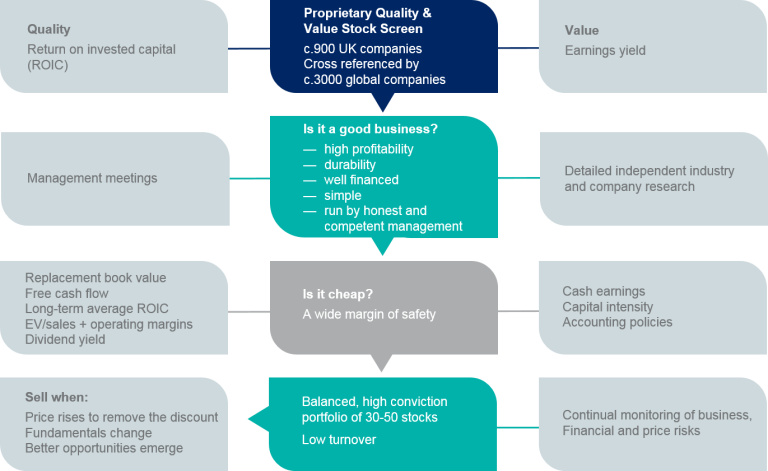

Investment process

The investment process is formed using ten core investment principles, and revolves around the three areas of risk management, quality and value. Risk management comes first because our understanding of this concept directs our stock selection.

Risk Management

A risk-based approach is aimed at minimising risk to maximise returns. Risk is defined as a permanent loss of capital and derives from three principal sources: deteriorating earnings power (business risk), too much debt (financial risk) and overpaying (price risk).

Quality

Business and financial risks are minimised by investment in a narrowly defined group of companies that exhibit:

— High profitability

— Durability

— Low leverage

— Simplicity

— Honest and competent management.

Value

Good investments are made when quality companies are purchased at attractive valuations, thereby minimising price risk. Ideas are generated through a number of sources including a proprietary screen of stocks. All investments undergo intensive due diligence which gives us the confidence to make significant investments in a select group of best ideas.

Process flow

Mainstream markets are large, well-followed and liquid. Many heavily incentivised, educated investors scrutinise the same information, and their actions and diverse opinions quickly incorporate news into asset prices. Mispricings are rare and rough efficiency is the norm. However, discrepancies do happen in individual shares, sectors, and whole markets. Investors are not the ‘rational actors’ described in finance theory textbooks, who can calculate risk in terms of prospective return. We are in fact driven by powerful psychological habits that induce collective bouts of poor decision-making. Greed, fear, and envy occasionally cause us to buy what is going up and sell what is going down, the exact opposite of ‘buy low, sell high’. At the extremes, asset ‘bubbles’ form and ‘pop’ under the force of mass irrationality. The existence and correction of market inefficiencies is one of the most dependable elements in investment markets. For those able to exploit them, they are the raw material for outperformance.

Investors must act differently from the rest of the market if they are to outperform. They also need to be right. Greater speed, hard work, and intelligence, are useful in making correct non-consensus decisions. However, there are plenty of investors with these attributes who still fail to add value. To run against consensus and get it right, you must have superior insights from better information, analysis, or both. You need an edge. This requires independence, scepticism, and patience. Above all, it requires a disciplined and repeatable investment process carefully designed to take advantage of market inefficiencies when they appear.

Idea Generation

The vast majority of research is conducted internally, and all decisions are based on the investment principles described above. Although the process is more qualitative than quantitative, screens are used at a preliminary stage to help in the discovery of new opportunities. They are also used extensively to monitor the relative attractions of existing investments. In particular, a proprietary Quality & Value Screen ranks all stocks into quintiles. The top quintile contains shares with the highest returns on capital (highest quality) and the highest earnings yield (greatest value). The same screen is run for the UK, Europe and global markets. This global framework helps to compare assets within sectors and between them.

Many financials and all utilities are removed from the screen since differences in their capital structures make their inclusion problematic for comparison purposes. For these sectors, earnings yield, return on equity, tangible book value, and various sector-specific measures of solvency and profitability are used as initial screens for quality and value.

In addition to proprietary screens, other filters are used to narrow our universe of stocks. These include identifying companies with:

— High dividend yields.

— Low price-to-book values.

Newspaper stories and stockbroker research help us to pick up the ‘scent’. Opportunities can stare contrarian investors in the face because negative headlines beget negative sentiment which is often reflected in share prices. A handful of trusted stockbroker contacts who know our methods occasionally provide us with a lead. Meetings with company management teams will also provide fresh insight into competitors and companies in related industries.

Screening is the beginning of a much longer research effort during which many subjective filters are applied. Once a stock idea is identified, the investment process becomes intensive and includes meeting company management and industry experts; hours and hours reading corporate report and accounts, and the thorough review of historic financial data. External research is used to cross reference our own work, especially for larger companies.

The investment process makes a virtue of understanding a company’s long-term operating and corporate history. Bloomberg and Canaccord Genuity’s Quest platform are important sources for this kind of company data.

Sell discipline

When a stock is purchased, it is our intention to own it for as long as it continues to fit our investment criteria. We never count on making a good sale. Instead we focus on making purchases so good that even a poor sale gives reasonable results. Generally speaking, a stock is sold for the following reasons:

- The margin of safety becomes too small, either because the stock price increases to eliminate the attractive discount (rising price risk) or the fundamentals change (higher business or financing risk).

- When better opportunities are found elsewhere.

Furthermore, we run a “suspect screen” on a monthly basis. The screen identifies stocks that have experienced both analyst downgrades and relative share price underperformance. Three consecutive appearances trigger a formal review by a member of the team.